Real Proposal: Propel vs. Participate on the Same House

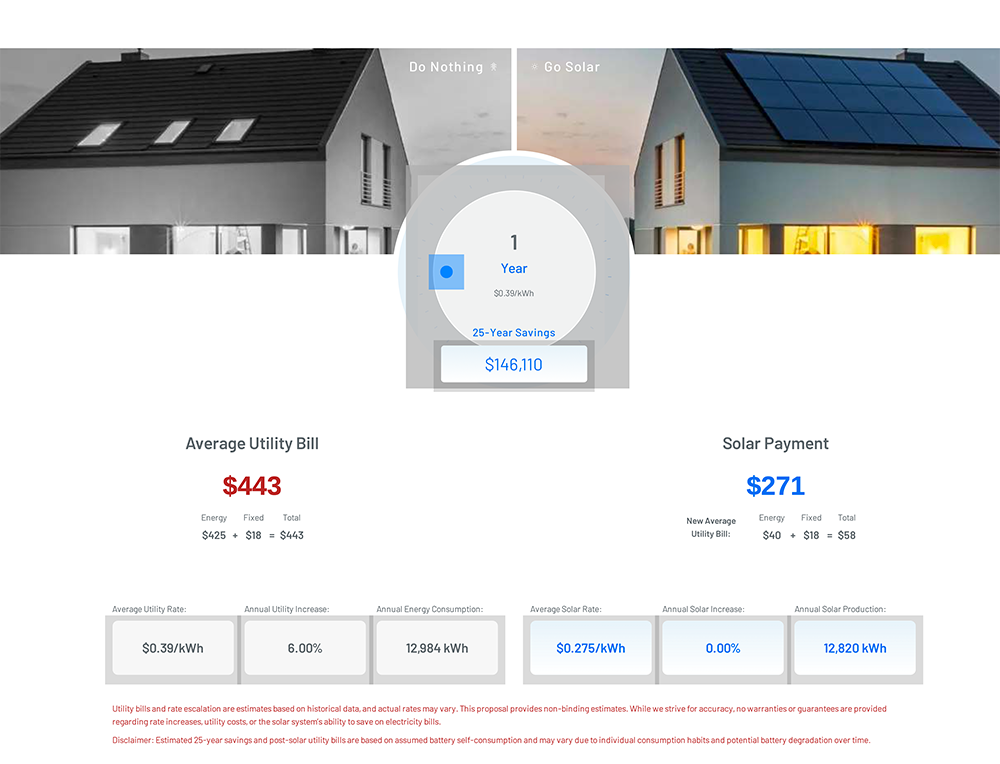

These are actual proposal screenshots from a single Southern California home. Same 7.38 kW system, same 18 panels, same $426/mo utility bill at $0.51/kWh. Two different programs, two different numbers. This is what a side-by-side comparison actually looks like.

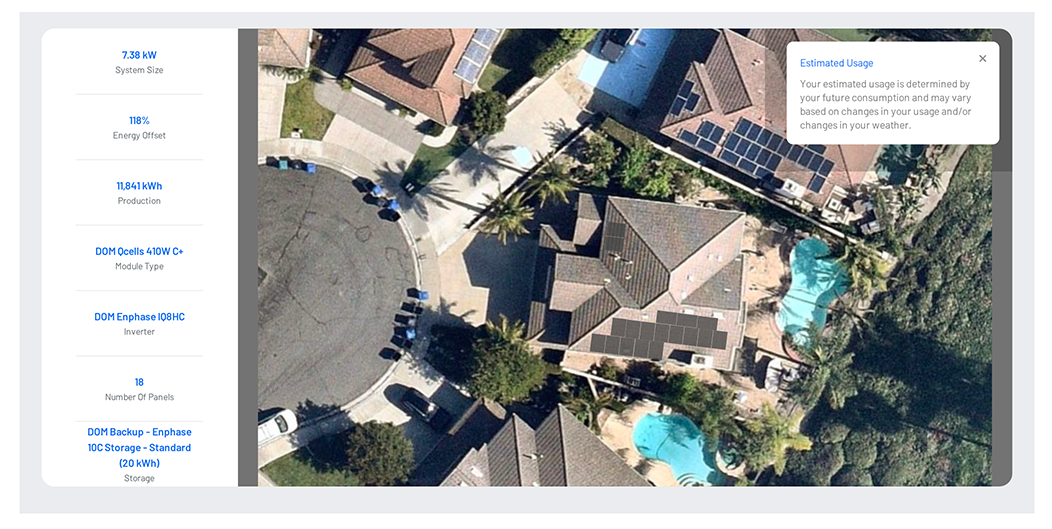

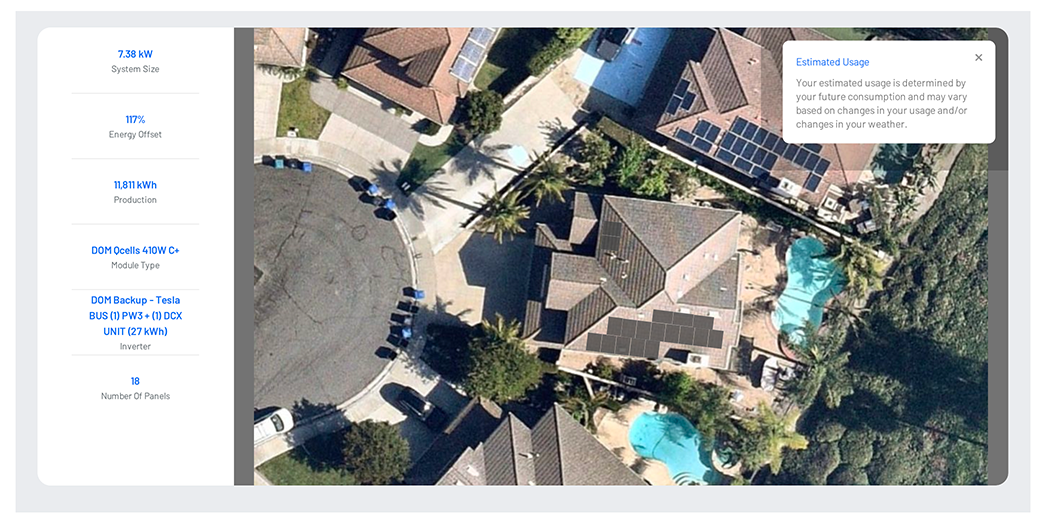

System Design

Both proposals show the same rooftop and system size. The hardware differs: Propel uses Enphase IQ8HC microinverters with Enphase IQ Battery 5P storage. Participate uses Tesla Powerwall 3 with DCX expansion. The lower Tesla PW3 hardware cost is what brings Participate's starting system price in lower.

Same home, same roof, same 18 panels. Propel shows Enphase IQ8HC + IQ Battery 5P (20 kWh). Participate shows Tesla Powerwall 3 + DCX unit (27 kWh total storage). The PW3's integrated inverter and higher capacity per unit is why the starting system price differs between proposals.

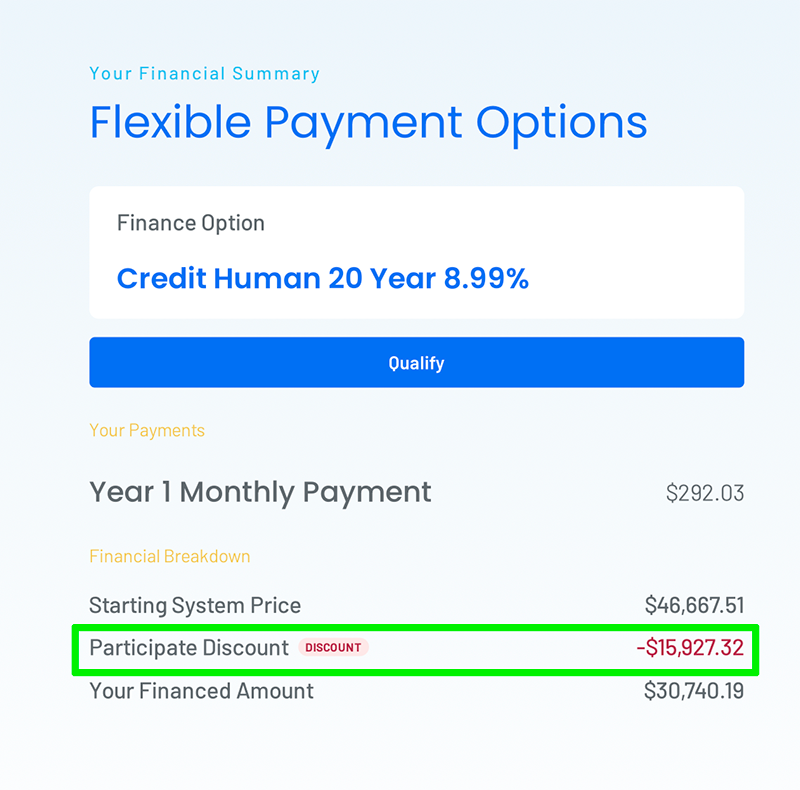

Financial Breakdown at Signing

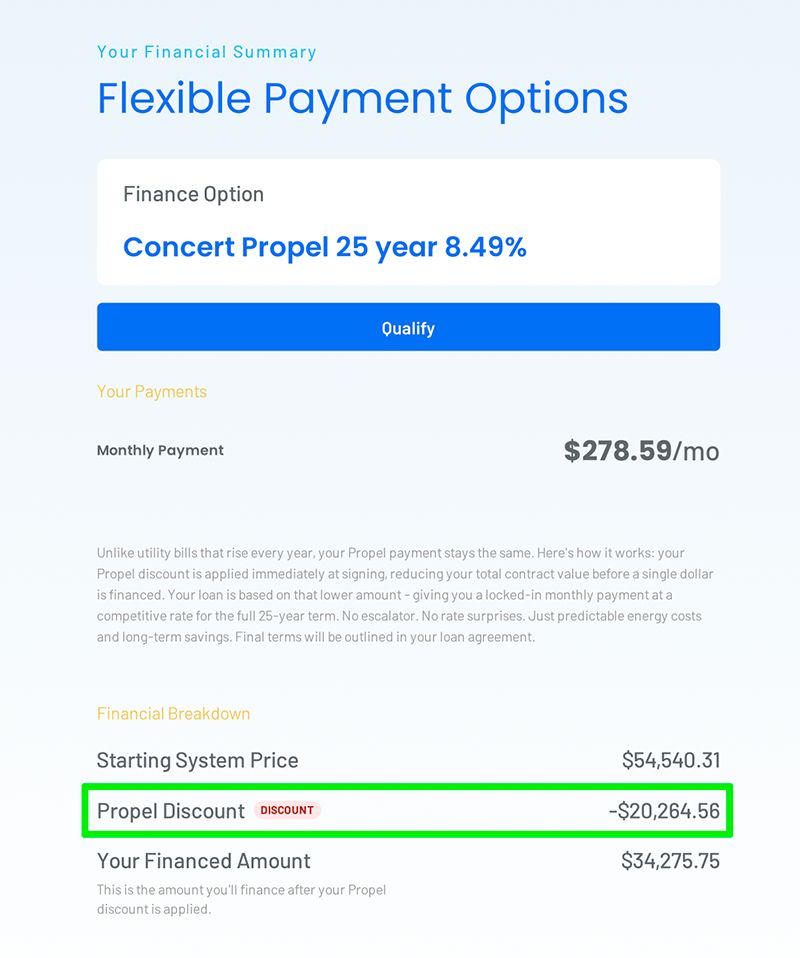

This is the most important comparison. Both proposals show the starting system price, the discount applied before financing, and the financed amount that becomes the loan balance. The address is not in an Energy Community, so both discounts are at the standard tier.

Propel: $54,540 starting price minus $20,264 discount (37.2%) = $34,275 financed at 8.49% APR, 25 years = $278.59/mo. Participate: $46,667 starting price minus $15,927 discount (34.1%) = $30,740 financed at 8.99% APR, 20 years = $292.03/mo. The lower Participate starting price is what makes its effective rate competitive despite the higher APR.

Monthly Bill Comparison

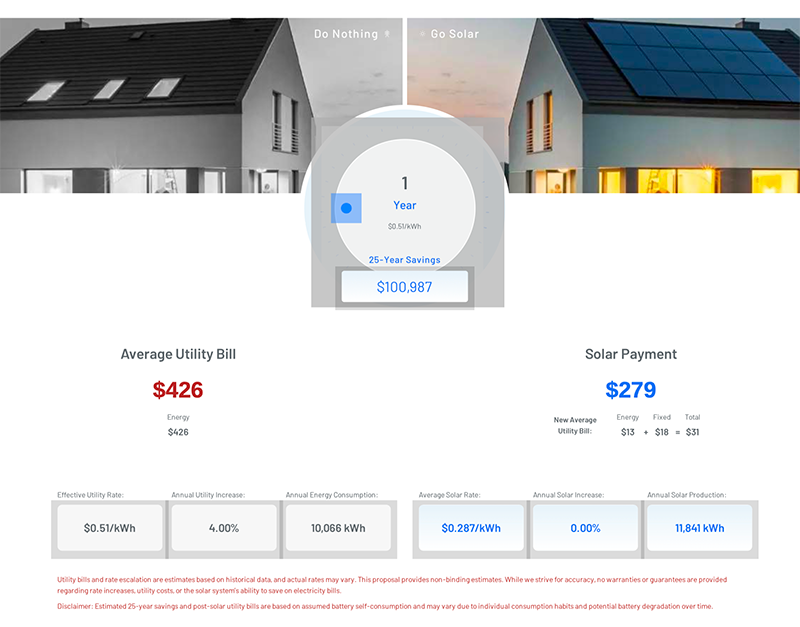

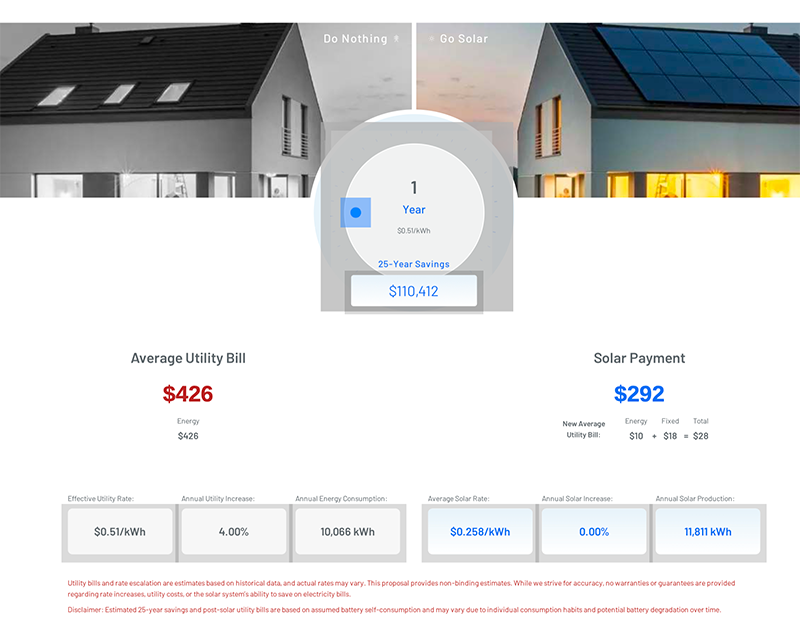

Both proposals show the same $426/mo utility bill before solar. Here is what the new monthly picture looks like under each program. The solar payment replaces most of the utility bill, with a small residual charge remaining for grid connection and any excess usage.

Propel: $279/mo loan payment + ~$31 residual utility = ~$310 total. Participate: $292/mo loan payment + ~$28 residual utility = ~$320 total. Both are meaningfully below the $426 utility-only baseline, with no escalation on the solar payment for the full loan term.

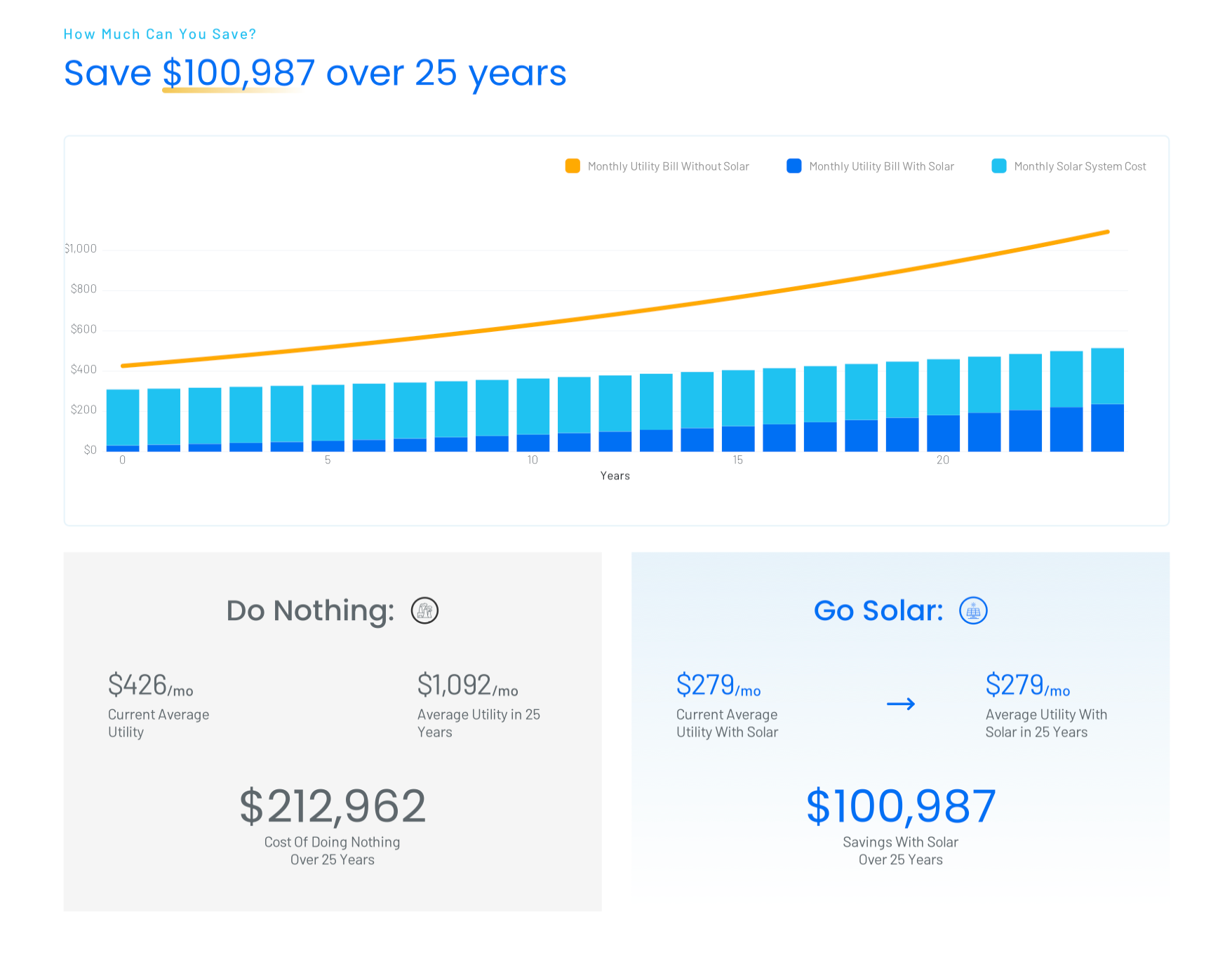

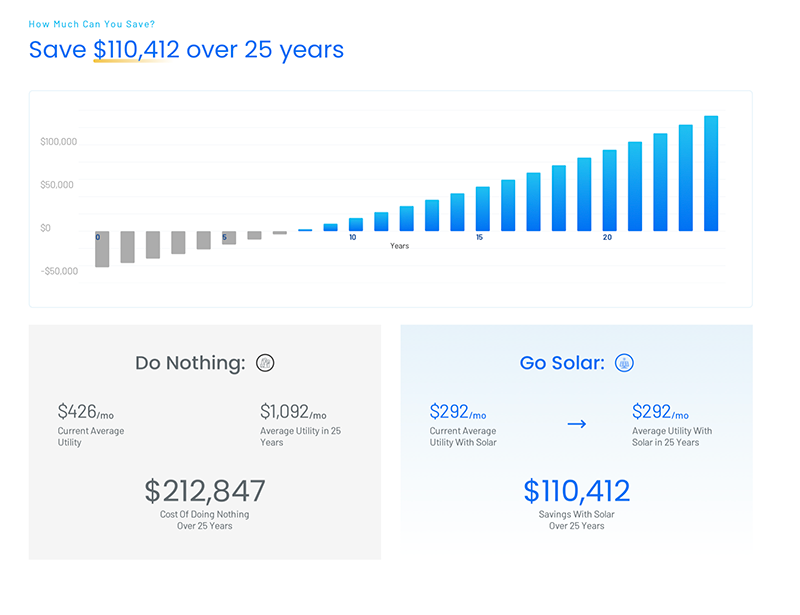

25-Year Savings

Both charts assume the same utility rate escalation at 4%/yr. The solar payment stays fixed while the utility comparison line keeps climbing. The result is a widening savings gap every year. Because this address is not in an Energy Community, Participate's lower starting system price produces a better 25-year savings outcome despite the higher APR.

On this non-Energy Community address, Participate saves $9,425 more over 25 years than Propel. In an Energy Community zip code, the 39.2% Propel discount would shift this outcome the other direction. This is why we run both quotes before presenting a recommendation.

| Data Point | Propel (Enphase) | Participate (Tesla PW3) |

|---|---|---|

| Starting System Price | $54,540 | $46,667 |

| Discount Applied | $20,264 (37.2%) | $15,927 (34.1%) |

| Financed Amount | $34,275 | $30,740 |

| Loan Rate / Term | 8.49% / 25 years | 8.99% / 20 years |

| Monthly Solar Payment | $278.59 | $292.03 |

| Residual Utility Bill | ~$31/mo | ~$28/mo |

| Total Monthly Energy Cost | ~$310 | ~$320 |

| Battery Storage | Enphase IQ Battery 5P (20 kWh) | Tesla PW3 + DCX (27 kWh) |

| 25-Year Savings (non-EC zip) | $100,987 | $110,412 ▲ |

| Winner on this address | Non-EC zip favors Participate | Better here |

This address is in Mission Viejo, CA (SCE territory) and is not in a federally designated Energy Community zip code. In an Energy Community zip code, Propel's 39.2% discount would reduce the financed amount further and flip the savings comparison. We verify Energy Community status using the Baker Tilly tool at the project address level before presenting program recommendations.