A Closer Look at Each Financing Path

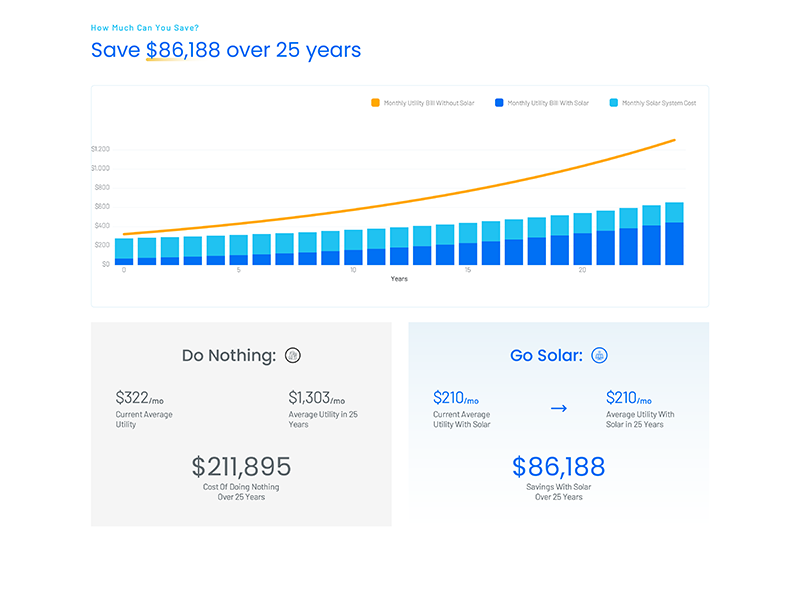

For a typical California solar home with an electric bill between $250 and $400+ per month. See our California solar incentives page for programs that stack with all financing options.

⚡ The Propel Loan by Concert Finance

Best in Energy Community zip codes

The Propel Loan by Concert Finance starts with a discount applied before a single dollar is financed. Concert holds commercial ownership for five years, unlocking commercial-grade clean energy tax credits and MACRS accelerated depreciation. That combined benefit is passed to the homeowner as a 30 to 39.2% reduction off the system price, which becomes the actual financed amount. The loan is then a 25-year fixed-rate product with no escalator, no dealer fee, and no prepayment penalty. Hardware is Qcells 410W panels with Enphase IQ8HC microinverters and Enphase IQ Battery 5P storage.

⚡ Participate Energy Prepaid Lease

Best outside Energy Community zip codesThe Participate Prepaid Lease uses the same Concert Finance commercial ownership structure as Propel, but the financing is through Credit Human at a 20-year term. Hardware is Qcells 410W panels with Tesla Powerwall 3 as the standard battery. Because the Powerwall 3 integrates the solar inverter and battery in one unit, the starting system price is typically lower than a comparable Enphase system. In standard zip codes where the discount stays at 30%, that lower starting price often results in a better monthly payment and 25-year savings outcome than Propel. Participate also has no FICO minimum and no UCC lien.

Cash Purchase

Best lifetime ROI if capital is availableA cash purchase means paying the full system cost upfront with no loan. There are no ongoing financing payments, so every dollar of utility savings accumulates without offset. This path delivers the highest 25-year net savings of any option, but it requires significant capital on day one and the break-even period is typically around year 10.

PPA (Power Purchase Agreement)

Lower barrier, no ownershipWith a PPA, the homeowner pays for the electricity the solar system produces rather than owning the system itself. There is usually little or no upfront cost, which lowers the barrier to entry. The tradeoff is no ownership, and annual escalator clauses typically 2 to 3% per year mean the savings gap narrows over time.

No Solar

Typically the most expensive 25-year outcomeStaying on utility power with no solar means no upfront cost, but also no protection from rate increases. California utility rates have risen consistently, and with no solar system generating energy, the homeowner remains fully exposed to escalation. Over 25 years, this path typically produces the highest cumulative energy spend of any option on this list.