The residential solar tax credit expired at the end of 2025. Propel by Concert Finance uses a commercial ownership structure to capture that credit value and pass the savings directly to you as an upfront discount before a single dollar is financed.

Concert Finance uses a commercial ownership structure to unlock federal tax credits no longer available to residential homeowners. Those savings are passed to you as a real, upfront discount before any loan amount is set.

For years one through five, Concert Finance holds commercial ownership of the solar system. This structure qualifies the system for commercial-tier Investment Tax Credits unavailable to residential buyers.

The ITC value, typically 30-40% of system cost, is passed to you as an upfront discount before the loan is calculated. You borrow a genuinely reduced amount from day one, not an inflated one.

Your Propel payment is set at 7.79% APR over 300 months. No escalator, no dealer markup buried in the balance, no surprises at year five or year fifteen.

At the five-year mark, the system is yours outright. It adds to your home's assessed value and produces power at zero marginal cost for the remaining life of the panels.

Built by Concert Finance exclusively for authorized partners. These are terms your neighbors won't find on a standard solar loan application.

Applied before financing. 39.2% in IRS Energy Community zip codes. 29.8% in standard markets. Reflects the commercial ITC value passed directly to you.

7.79% APR, 300 months. Your Propel rate today is your rate in year 20. No escalator, no rate resets, no surprises.

Concert Finance holds temporary commercial title, then full ownership transfers to you at the five-year mark with no additional out-of-pocket cost.

Pay off the loan early at any time. Accelerate ownership on your schedule with zero exit fees.

Restructure the loan balance at months 12, 24, and 36. This is rare in the solar lending market and lets you lower your monthly payment with a lump-sum contribution.

Most solar loans inflate the financed amount with 20-30% dealer fees. Propel charges none. You borrow the real system cost.

A low year-one payment is not the same as the best 25-year outcome. Here is what the math actually looks like across the most common solar financing options available to California homeowners today.

| Feature | ⚡ Propel by Concert Finance | Traditional Solar Loan | Monthly PPA / Lease |

|---|---|---|---|

| Upfront cost to start | $0 to start | Often required or inflated | $0 to start |

| Upfront discount applied | 30-40% before financing | None | None to homeowner |

| Dealer fees in price | Zero dealer markup | Often 20-30% added | N/A |

| Payment escalation | Fixed for 25 years | Fixed | 1-3% per year common |

| System ownership | Transfers at year 5 | Immediate (inflated price) | May never own |

| Prepayment penalty | None | Often yes | N/A |

| Tax credit access | 30-40% via commercial structure | Residential ITC expired 2025 | Not available to homeowner |

| Credit check required | Yes, 660 FICO minimum | Yes, typically 680+ | Varies by provider |

| Home sale complexity | Simple, tied to borrower | Simple | Lease transfer required |

← Scroll on mobile to see all columns

These are real numbers from finalized Propel proposals. Monthly payments and discount amounts vary based on system size, utility territory, and Energy Community status.

Savings projections model 6% annual utility rate escalation based on historical CA averages. Actual results vary. Discount amounts are finalized at signing based on system size and zip code eligibility.

The federal Investment Tax Credit for commercial solar is 30% in most markets. In IRS-designated Energy Community zip codes, a 10% bonus adder raises the effective credit to 40%. Propel passes that full value to you as an upfront discount before any financing is calculated.

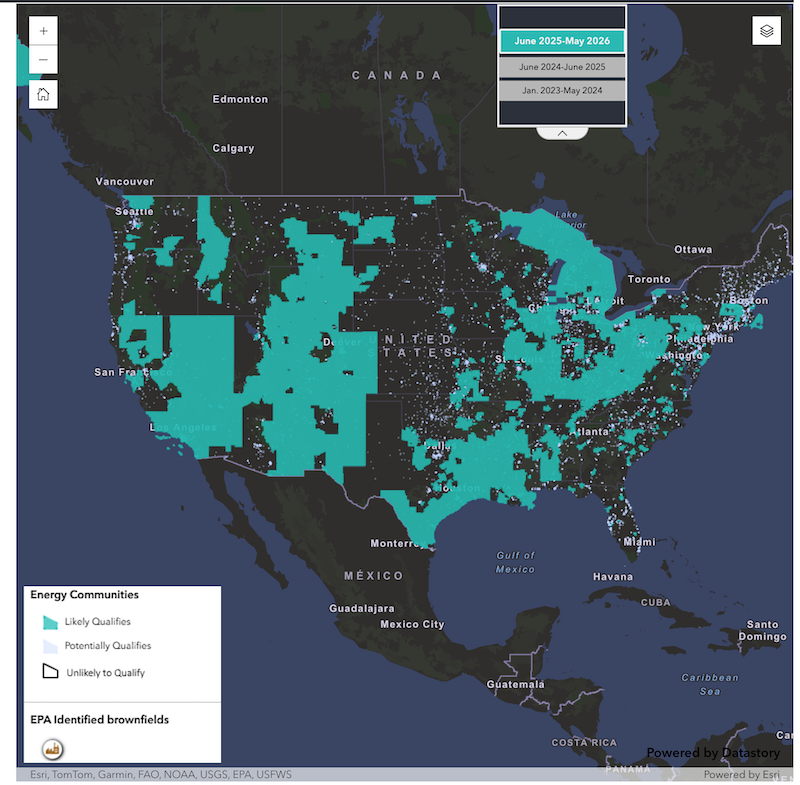

Homeowners in qualifying Energy Community zip codes receive the maximum Propel discount. These are areas historically associated with fossil fuel employment or coal mine closures, as defined by the IRS under the Inflation Reduction Act.

CA examples include parts of Kern County, Tulare County, and Kings County. Your advisor confirms your exact zip at application before the proposal is built.

In zip codes that do not qualify for the Energy Community adder, the base commercial ITC rate of 30% applies. Propel passes 29.8% of your system cost as an upfront discount before financing.

Most coastal California markets fall here, including much of the Bay Area, the Los Angeles metro (outside LADWP territory), and San Diego County.

IRS Energy Community designation map. EC zip codes unlock the 7% bonus adder, raising the Propel discount to 39.2%.

Get a custom Propel Financing proposal built from satellite imagery of your roof, your exact utility rate, and your actual energy usage. Free and specific to your home.